{kind=link}

OSLO – The global market share of electric vehicles is expected to grow so quickly that battery manufacturers cannot meet production requirements, an analysis by Rystad Energy shows.

This is because the mining capacity of lithium – a key component of batteries for electric vehicles – will lag behind demand unless investment in new mines accelerates. Under the current pipeline, capacity shortages could triple lithium prices by the end of this decade.

While today’s lithium mining capacities can easily meet the demand in the electric vehicle market, the rapid increase in electric vehicles will lead to a serious lithium supply deficit as early as 2027.

This imbalance will widen over the years and will result in delays in the production of millions of electric passenger cars, even if planned new mining projects increase their capacity in the years to come.

Further investment decisions for the construction of new lithium mining projects need to be added to the pipeline quickly, as Rystad Energy estimates that the development, financing and construction of an average new project can take anywhere from five to seven years.

Based on our current prospects for lithium mining capacity and the proportion of lithium demand that electric passenger cars will cause, we estimate that the supply deficit will delay the production of around 3.3 million electric vehicles with a battery of 75 kilowatt hours (kWh) as early as a year 2027.

The impact will quickly escalate to around 9 million electric vehicles in 2028 and around 20 million electric cars in 2030.

“A major disruption is brewing for the manufacturers of electric vehicles. Although a lot of lithium needs to be mined in the ground, the existing and planned projects will not be enough to meet the demand for the metal.

“If the pipeline does not expand rapidly with more mining projects, the energy transition in road transport may have to slow down,” said James Ley, senior vice president of Rystad Energy’s Energy Metals team.

In addition to electric passenger cars, the expected capacity deficits in lithium mining will also disrupt the production lines of other vehicles that are fully or partially electrified and require batteries such as buses, trucks and hybrid cars.

Demand from the shipping and aviation industries as well as from grid storage will also feel the lithium shortage.

While lithium-ion isn’t the only battery technology, it is vastly superior in EV applications and will not be replaced by anything else this decade.

Even if other technologies later evolve, lithium is likely to be used as well, albeit possibly in smaller amounts. Lithium is the lightest metal suitable for batteries. If you swap it out for something else, it will lower the energy density, resulting in shorter ranges for electric vehicles.

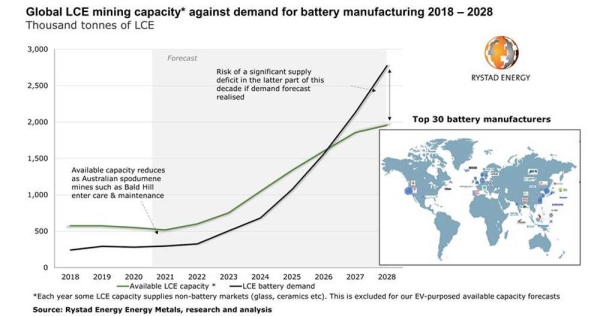

Excluding the lithium mining capacity that supplies non-battery markets such as glass and ceramics, the remaining lithium production capacity that can be used to make batteries of all applications in 2021 is nearly 520,000 tonnes of lithium carbonate equivalent per year.

Widely known as the LCE, this device is the most widely used measure of lithium production on the market.

Battery manufacturers’ demand for LCE is estimated at around 300,000 tons this year, but it will increase rapidly.

As early as 2025, battery manufacturers’ LCE demand will reach just over 1 million tons, compared to an LCE mining capacity of just over 1.3 million tons if other uses are excluded. By 2026, the order of magnitude will tend towards a small deficit in mining capacity.

If the current pipeline of the mining project is left unchanged, the capacity deficit will increase and reach nearly 820,000 tons in 2028, when LCE demand is estimated at 2.8 million tons.

The situation could get even worse as demand continues to rise and the imbalance may rise to 2 million tonnes of LCE as early as 2030.

LCE prices averaged around $ 8,200 per ton in 2020. The metal’s value rose massively a few years ago from $ 6,500 / tonne in 2015 to a record high of $ 17,000 / tonne in 2018, before the market began to calm down in 2018 by the end of the year and through to 2019.

“We anticipate lithium prices could repeat their previous turmoil if supply fails to catch up with booming demand for electric vehicles later this decade. With the important task ahead of building more mining capacity, prices could even triple due to the market imbalance, ”added Ley.

The 160% price hike in 2015-18 was mainly due to increasing demand for electric vehicles from China and a temporary shortage of lithium.

In contrast, lithium carbonate prices fell back to 2016 levels over the past year and almost hit breakeven for mega-producers in China as supply soared to meet demand and the pandemic slowed global production.

Is lithium recycling an option?

In the long term, structural changes appear to be necessary to make the lithium industry sustainable.

Mining itself, which appears to be the only short-term option to cover supply, is increasingly at risk of derailing the environmental permits that the EV industry seeks to embody.

Lithium mining in hard rock requires large amounts of water and can release up to 15 tons of CO2 per ton of lithium produced.

The extraction of lithium from brine deposits, while omitting less CO2 than rocks, requires even more water and often takes place in parts of the world where water is scarce.

As the electric vehicle industry matures, industries need to be built and cultivated that encourage the use of second-life batteries and near 100% recyclability.

Battery recycling has been blocked by technical limitations, economic barriers, logistical problems and regulatory loopholes.

The current recycling of batteries requires high temperature melting and extraction or melting processes that are energy intensive and not environmentally friendly.

A major problem was that batteries were not designed with material recovery in mind, only to produce energy for a long time and as cheaply as possible.

As battery recycling becomes more important, startups in America and Europe are beginning to commercialize new battery recycling technologies.

We believe that the fight against recycling will increase as more batteries reach the end of their life.

However, widespread adoption of battery recycling may not be seen until after 2030, as EV batteries currently entering the system typically have a 15 year lifespan.

It is therefore unlikely that recycling will fill the lithium supply gap for battery manufacturers after 2025.

We therefore expect lithium prices to rise in line with our demand forecast until new mines are developed beyond the 40 currently proposed. – Rystad Energy